Jamie – Year 12 Student

Editor’s note: Talented economist Jamie, now in Year 13, writes once again for the Humanities Journal, examining whether now is the time to implement a Mansion Tax. He tackles three key points: the issues with the taxation of property, the under taxation of wealth and widening economic inequality. He neatly draws together strands of argument to reach a well-considered and meticulously researched conclusion. This is Jamie’s fourth publication in The GSAL Journal; click here to view his other contributions. Mei – Chief Editor, Humanities Journal

The Mansion Tax is defined as an annual levy of 10% of the excess value above £2 million of any property – a high threshold that compromises revenue in order to better address inequality. This proposal purports to redress three issues: the issues with the taxation of property, the under taxation of wealth and widening economic inequality. If it can address these pressing issues, its time has come.

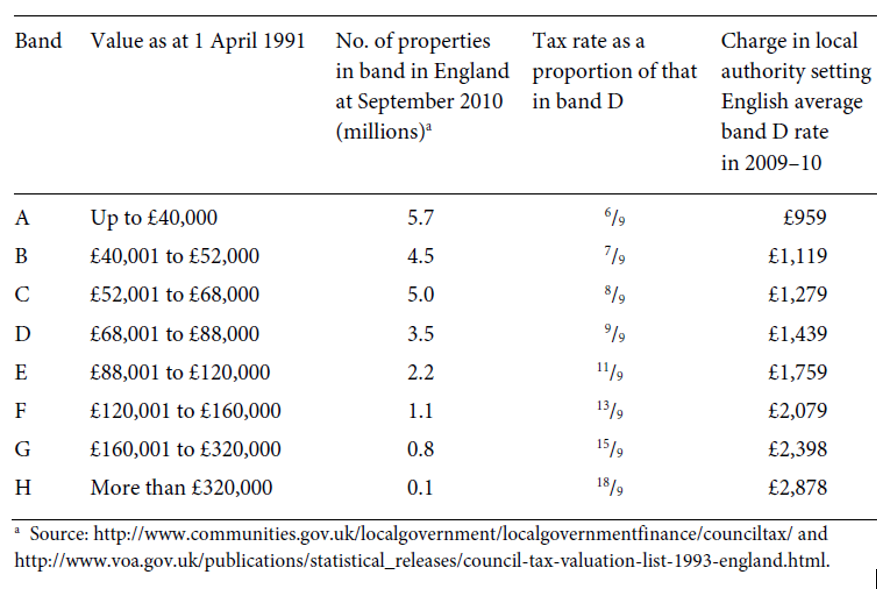

Fig.1 (IFS 2012)

Council Tax is regressive – Fig. 1[1] shows that at the top of Band A 2.4% of house value is taxed annually, compared to 0.75% for the top of Band G. A higher proportion of a poorer household’s wealth is taxed annually; this is a regressive replacement to the reviled Poll Tax. The failure to revalue property since 1991 means houses are not taxed in accordance with their current value, due primarily to home improvement and changes in regional prosperity since 1991. Regional variation in rates creates inequity and a geographical lottery. Moreover, the fact the South East has higher nominal incomes and higher house values but the same bands means that in real terms Council Tax is lower in these wealthier areas, particularly given Council Tax does not differentiate between a £320,000 family home and a £15 million mansion. Stamp Duty is a poor solution – it disincentivises mutually beneficial housing transactions, reducing total societal utility. Thus, it does not meet the fifth canon of tax because it adversely affects decision making and doesn’t support economic activity. Consequently, the time has come for a reformation of property taxation.

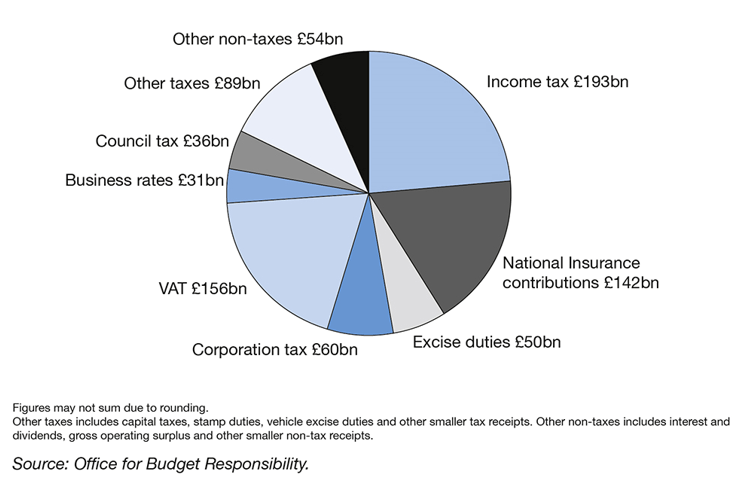

Fig. 2 [2] (Budget 2018, 2020)

A new tax should provide desirable economic incentives. Fig 2 shows that taxes on economic activity – income and consumption taxes – entail around 75% of the tax burden. The top income earners already pay 45% Income Tax and 12% NI (the top 1% account for 30% [3]of income tax takings (IFS)); it seems hard to increase rates without reaching the peak of the Laffer curve. Increased takings would not incentivise work and impede macro-economic performance, reducing revenues (Mitchell, 2020)[4]. Moreover, too few pay the top rate for a small increase to generate meaningful extra revenue. Taxation of wealth is desirable as it is clearly undertaxed under the status quo, but also because value accrues to owners of wealth largely independently of their activity (particularly in property, the wealth in question). Thus, taxation of wealth does not affect the incentives of the owners. Given wealth must be taxed, it seems egregious not to target housing. Housing wealth in the UK in 2009 was £3.5 trillion, set against £3.7 trillion for all other financial assets (IFS 2012). The 72% of homes that are owner occupied (IFS 2012) do not even pay Capital Gains Tax. Housing wealth dwarfs other assets and is not taxed sufficiently or progressively.

Housing could be taxed annually or even as a one-time levy on property such as that which David Ricardo proposed to pay £800 million[5] (O’Brien 1989) (in 1815 – 100s of billions today) of the national debt created by the Napoleonic and French Revolutionary Wars. A tax on property not only preserves incentives but would also be highly efficient. Property cannot be offshored or hidden, making it cheap and easy to administer. This also makes it easy for the taxman to see the revenue due. This is crucial: a new tax must be equitably administered.

The Mansion Tax preserves economic incentives – the utility derived from a mansion is unchanged, and given that there is little other use for the property it is exceedingly unlikely its usage will change. If the value of the tax will be capitalised into the sale price, incentives to purchase mansions will persist and thus incentives to build mansions will persist. This capitalisation means current owners will see an inequitable and arbitrary fall in the value of their property assets that future and past owners are exempted from. However, as Churchill noted defending a Land Value Tax in the “People’s Budget” in 1910, the value of land derives from its location and taxpayer investment in the area. For example in the UK, a good school can improve house values by 5-20% (Webb 2013)[6]. That which this economic rent accrues, unearned, to the homeowner while created by the taxpayer is inequitable. The average San Jose house price increased 3.7 times 1996-2016 (Economist 2018)[7]; this is patently not due to the owner. Rising house prices have made owners rich off societal efforts; it is equitable to recoup that wealth for the society that created it.

To be equitable, a tax must provide for the prevention of injustices. While asset-rich, cash-poor pensioners may struggle to pay, tax payment could be deferred until death to avoid forcing people out of their homes. In order to begin immediately redistributing wealth, this deferment would only be available on a means-tested basis. A further issue is that the top 0.1% hold 80% of their wealth in bonds and equities (Wolf 2018)[8]: housing wealth is of greater import to the middle class than the richest of society. This indicates the Mansion Tax will take a higher proportion of the wealth of the middle classes, thus failing to reduce inequality. However, this is avoided by having a high threshold for the Mansion Tax, and then placing a high rate above that e.g. the 16% levied in Singapore (Webb 2013) to ensure the super-rich are being taxed. I am proposing a rate far below this, but a higher rate and higher threshold than any UK political party has advocated. This would also largely redress the issue of pensioners. A final potential inequity lies in flawed normative judgments of house value. This has the potential to create unfair incidence of tax and to give rise to a litany of appeals and court cases that could erode the efficiency of the tax. Such has not occurred in the levying of Business Rates on extremely wealthy and legally well-equipped corporations; the property market relies on the reliability of independent valuations of houses and it seems unlikely that a significant amount of such errors will suddenly occur when the evaluation is for a tax not a sale.

Fig 3

The extra tax revenue allows for investment in infrastructure (quantity of capital increases), education (quality of labour increases) and other long term capital spending which pushes the LRAS to the right by increasing the quality and quantity of factors of production, facilitates long run growth and increases living standards – particularly for the poor. This redressing of societal inequity and suffering outweighs the inequity created by exceedingly rare cases of flawed valuations.

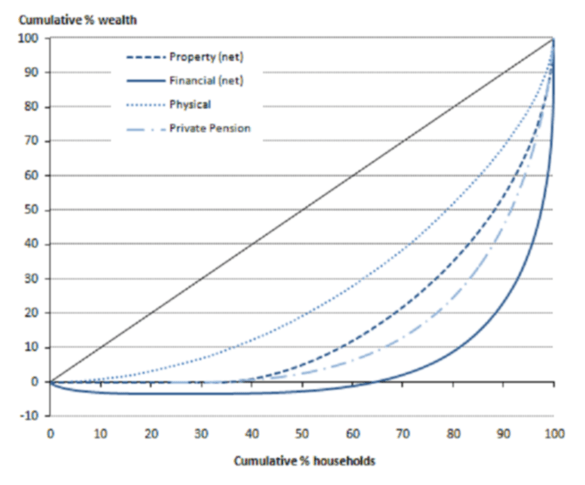

Fig.4 (ONS 2015)[9]

Inequality is rising; the time has come to mitigate it. The UK’s top 10% own 45% of national wealth; the poorest 10% own 2%. This is burgeoning gap is widening: the top decile’s wealth grew four times faster than the bottom’s in 2018 (Inman 2019)[10]. The UK’s Lorenz curve (Fig 4) is illustrative of this uneven distribution of wealth. It is for 2012-14; the issue has worsened in the last 6 years. Taxing top incomes carries the issues discussed earlier. However, the Mansion Tax entails wealth redistribution while providing the desirable property tax already discussed. It starts to redress the harmful effects of inequality: crime, social unrest, poorer health outcomes, unequal allocation of political power and uncompetitive markets[11]that economists like Stiglitz (2013) are particularly concerned about. A higher rate of Council Tax on properties above a threshold could turn it from regressive to progressive, particularly if with the revenue, the burden on low income households was reduced. Levying a proportion of value would also impose a higher nominal tax in more prosperous areas of higher property values, and thus an equitable real burden. It could also replace Stamp Duty, and thus restore economic incentives to engage in utility-maximising transactions. Finally, re-valuation of property to see if it meets the threshold for Mansion Tax would be a politically tenable way to move the Council Tax system off 1991 valuations.

Increased taxation of the wealthy is needed to limit growing inequality. Given the high taxation of economic activity in the UK already, a tax on wealth seems far less likely to damage economic incentives than further taxation of income, and property is the best option. This is because it dwarfs other forms of wealth, is immobile, and is hard to conceal, thus rendering the tax efficient and likely to fall equitably, even on those with expensive lawyers. This tax should fall on mansions to meet the long – term need to redistribute wealth and redress a growing wealth gap, a long standing need to reform an increasingly flawed system of property taxation and a need to address the inequitable accruement of unearned economic rent to landowners – an issue bemoaned from Henry George to Churchill. Detractors list practical objections but Denmark’s LVT shows taxation of land is possible and there is no reason why highly valuable residential land should differ. The time has come to levy Friedman’s “least bad tax” on the ever – increasing wealth of the uber wealthy.

References

Ifs.org.uk. n.d. [online] Available at: <https://www.ifs.org.uk/uploads/mirrleesreview/design/ch16.pdf> [Accessed 25 May 2020].

Ifs.org.uk. n.d. [online] Available at: <https://www.ifs.org.uk/uploads/BN259-How-high-are-our-taxes-and-where-does-the-money-come-from.pdf> [Accessed 6 June 2020].

GOV.UK. 2020. Budget 2018. [online] Available at: <https://www.gov.uk/government/publications/budget-2018-documents/budget-2018> [Accessed 4 June 2020].

Ons.gov.uk. 2015. Chapter 2: Total Wealth, Wealth In Great Britain, 2012 To 2014 – Office For National Statistics. [online] Available at: <https://www.ons.gov.uk/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/compendium/wealthingreatbritainwave4/2012to2014/chapter2totalwealthwealthingreatbritain2012to2014> [Accessed 3 June 2020].

Inman, P., 2019. Gap Between Rich And Poor Grows Alongside Rise In UK’s Total Wealth. [online] the Guardian. Available at: <https://www.theguardian.com/news/2019/dec/05/gap-between-rich-and-poor-grows-alongside-rise-in-uks-total-wealth> [Accessed 1 June 2020].

Mitchell, D., 2020. The Laffer Curve Wreaks Havoc In The United Kingdom. [online] Forbes. Available at: <https://www.forbes.com/sites/danielmitchell/2012/07/02/the-laffer-curve-wreaks-havoc-in-the-united-kingdom/> [Accessed 6 June 2020].

Stiglitz, J., 2013. The Price Of Inequality. New York: W.W. Norton & Company.

The Economist. 2018. The Time May Be Right For Land-Value Taxes. [online] Available at: <https://www.economist.com/briefing/2018/08/09/the-time-may-be-right-for-land-value-taxes> [Accessed 23 May 2020].

O’Brien, Patrick Karl. “The Impact of the Revolutionary and Napoleonic Wars, 1793-1815, on the Long-Run Growth of the British Economy.” Review (Fernand Braudel Center), vol. 12, no. 3, 1989, pp. 335–395. JSTOR, www.jstor.org/stable/40241130. Accessed 29 Mar. 2020

Webb, M., 2013. How A Levy Based On Location Values Could Be The Perfect Tax. [online] Ft.com. Available at: <https://www.ft.com/content/392c33a6-211f-11e3-8aff-00144feab7de> [Accessed 4 June 2020].

Wolf, M., 2013. Reform Council Tax And Close The Generational Wealth Gap. [online] Ft.com. Available at: <https://www.ft.com/content/b66441e6-2b66-11e8-9b4b-bc4b9f08f381> [Accessed 6 June 2020].

[1] Ifs.org.uk. 2012 [online] Available at: <https://www.ifs.org.uk/uploads/mirrleesreview/design/ch16.pdf> [Accessed 25 May 2020].

[2]GOV.UK. 2020. Budget 2018. [online] Available at: <https://www.gov.uk/government/publications/budget-2018-documents/budget-2018> [Accessed 4 June 2020].

[3] Ifs.org.uk. n.d. [online] Available at: <https://www.ifs.org.uk/uploads/BN259-How-high-are-our-taxes-and-where-does-the-money-come-from.pdf> [Accessed 6 June 2020].

[4] Mitchell, D., 2020. The Laffer Curve Wreaks Havoc In The United Kingdom. [online] Forbes. Available at: <https://www.forbes.com/sites/danielmitchell/2012/07/02/the-laffer-curve-wreaks-havoc-in-the-united-kingdom/> [Accessed 6 June 2020].

[5] O’Brien, Patrick Karl. “The Impact of the Revolutionary and Napoleonic Wars, 1793-1815, on the Long-Run Growth of the British Economy.” Review (Fernand Braudel Center), vol. 12, no. 3, 1989, pp. 335–395. JSTOR, www.jstor.org/stable/40241130. Accessed 29 Mar. 2020

[6] Webb, M., 2013. How A Levy Based On Location Values Could Be The Perfect Tax. [online] Ft.com. Available at: <https://www.ft.com/content/392c33a6-211f-11e3-8aff-00144feab7de> [Accessed 4 June 2020].

[7] The Economist. 2018. The Time May Be Right For Land-Value Taxes. [online] Available at: <https://www.economist.com/briefing/2018/08/09/the-time-may-be-right-for-land-value-taxes> [Accessed 23 May 2020].

[8] Wolf, M., 2013. Reform Council Tax And Close The Generational Wealth Gap. [online] Ft.com. Available at: <https://www.ft.com/content/b66441e6-2b66-11e8-9b4b-bc4b9f08f381> [Accessed 6 June 2020].- data is for US but presumably the UK is similar

[9] Ons.gov.uk. 2015. Chapter 2: Total Wealth, Wealth In Great Britain, 2012 To 2014 – Office For National Statistics. [online] Available at: <https://www.ons.gov.uk/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/compendium/wealthingreatbritainwave4/2012to2014/chapter2totalwealthwealthingreatbritain2012to2014> [Accessed 3 June 2020].

[10] Inman, P., 2019. Gap Between Rich And Poor Grows Alongside Rise In UK’s Total Wealth. [online] the Guardian. Available at: <https://www.theguardian.com/news/2019/dec/05/gap-between-rich-and-poor-grows-alongside-rise-in-uks-total-wealth> [Accessed 1 June 2020].

[11] Stiglitz, J., 2013. The Price Of Inequality. New York: W.W. Norton & Company.

Jamie 738526